Contatto

Contatto Come acquistare

Come acquistareConsegna

Guida all'acquisto

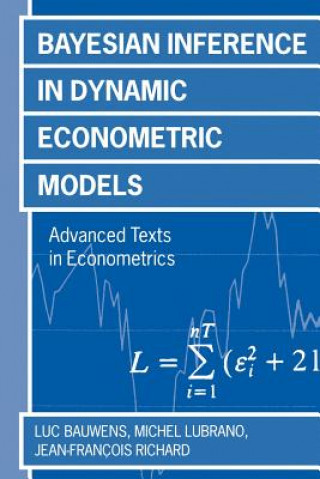

Bayesian Inference in Dynamic Econometric Models

Inglese

Inglese

225 b

225 b

30 giorni per il reso

I clienti hanno acquistato anche

/

/

Rigido

Rigido

29.59

€

29.59

€

/

In brossura

39.39

€

/

In brossura

39.39

€

This book contains an up-to-date coverage of the last twenty years advances in Bayesian inference in econometrics, with an emphasis on dynamic models. It shows how to treat Bayesian inference in non linear models, by integrating the useful developments of numerical integration techniques based on simulations (such as Markov Chain Monte Carlo methods), and the long available analytical results of Bayesian inference for linear regression models. It thus covers a broad range of rather recent models for economic time series, such as non linear models, autoregressive conditional heteroskedastic regressions, and cointegrated vector autoregressive models. It contains also an extensive chapter on unit root inference from the Bayesian viewpoint. Several examples illustrate the methods.

Informazioni sul libro

Inglese

Categorie

Regala questo libro oggi stesso

È facile

1 Aggiungi il libro al carrello e scegli la consegna come regalo 2 Ti invieremo subito il buono 3 Il libro arriverà all'indirizzo del destinatarioPotrebbe interessarti anche

/

In brossura

14.29

€

/

In brossura

14.29

€

/

In brossura

30.79

€

/

In brossura

30.79

€

/

Rigido

109.49

€

/

Rigido

109.49

€

/

In brossura

18.29

€

/

In brossura

18.29

€

/

In brossura

12.69

€

/

In brossura

12.69

€

/

Foglio

242.69

€

/

Foglio

242.69

€

Ciao! Sono Libroamiko, il tuo consulente di libri.

Come posso aiutarti?