Spedizione gratuita per ordini superiori a 69,99 euro.

Entra a far parte di una comunità di amanti dei libri di tutto il mondo e ottieni numerosi vantaggi.

Crea un account gratuito

Spedizione gratuita con Packeta per un prezzo superiore a 69.99 €

Corriere Bartolini 4.49 €

Punto Poste 5.49 €

Punto Poste 5.49 €

Punto Bartolini 3.49 €

Corriere DHL 6.99 €

Corriere GLS 5.99 €

Punto GLS 4.49 €

Contatto

Contatto Come acquistare

Come acquistare

Aiuto

Consegna

Corriere Bartolini 4.49 €

Punto Poste 5.49 €

Punto Poste 5.49 €

Punto Bartolini 3.49 €

Corriere DHL 6.99 €

Corriere GLS 5.99 €

Punto GLS 4.49 €

Spedizione gratuita con Packeta per un prezzo superiore a 69.99 €

Guida all'acquisto

Il mio account

▸

Vuoto :-(

0

Spedizione gratuita per ordini superiori a 69,99 euro.

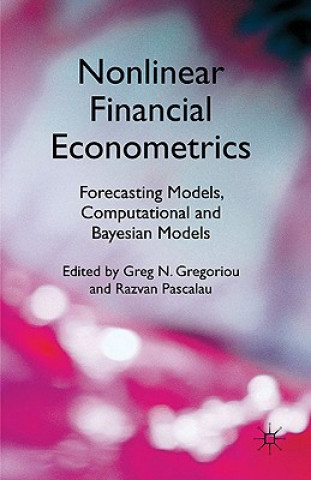

Nonlinear Financial Econometrics: Forecasting Models, Computational and Bayesian Models

Lingua

Inglese

Inglese

Inglese

Libro

Rigido

This book assesses several competing forecasting models for interest rates, financial returns, and r...

Descrizione completa

Codice Libristo: 04553467

?

141 b

141 b

141 b

57.79

€

Magazzino esterno in piccole quantità

Inviamo tra 13-18 giorni

Fino a 30 giorni per il reso

I clienti hanno acquistato anche

/

/

In brossura

In brossura

21.89

€

21.89

€

/

In brossura

28.09

€

/

In brossura

28.09

€

/

In brossura

20.99

€

/

In brossura

20.99

€

This book assesses several competing forecasting models for interest rates, financial returns, and realized volatility. In particular, the book proposes new forecasting tools; for instance, an iterative outlier detection procedure to detect and handle outliers in models for the volatility. In addition, the book discusses in detail the construction of optimal portfolios based on out-of-sample forecasting techniques. It also addresses the effectiveness of hedging in futures markets and proposes a Bayesian framework to explain the rate spreads on corporate bonds.

Attrice

&

Poliglotta

EWA KASP

per

Riproduci video

Libristo ha la più grande selezione di letteratura in lingue straniere. Per questo compro i miei libri qui.

Informazioni sul libro

Titolo completo

Nonlinear Financial Econometrics: Forecasting Models, Computational and Bayesian Models

Autore

G. Gregoriou, R. Pascalau

Lingua

Inglese

Inglese

Rilegatura

Libro - Rigido

Data di pubblicazione

2010

Numero di pagine

195

EAN

9780230283657

ISBN

0230283659

Codice Libristo

04553467

Casa editrice

PALGRAVE MACMILLAN

Peso

410

Dimensioni

143 x 223 x 17

Categorie

Regala questo libro oggi stesso

È facile

1 Aggiungi il libro al carrello e scegli la consegna come regalo 2 Ti invieremo subito il buono 3 Il libro arriverà all'indirizzo del destinatarioPotrebbe interessarti anche

/

Rigido

36.59

€

/

Rigido

36.59

€

/

In brossura

54.09

€

/

In brossura

54.09

€

/

In brossura

6.69

€

/

In brossura

6.69

€

/

In brossura

19.99

€

/

In brossura

19.99

€

/

In brossura

8.39

€

/

In brossura

8.39

€

Consulente di libri Libroamiko

Utilizzando questa chat, stai comunicando con un'intelligenza artificiale generativa. Utilizzandola, accetti anche il trattamento dei dati personali.

Ciao! Sono Libroamiko, il tuo consulente di libri.

Come posso aiutarti?

Ciao, sono Libroamiko, posso aiutarti?